Logistics Segments That Attract Investments

For an investor, knowing where the real value lies in logistics requires more than just tracking overall industry growth or chasing high-growth industries.

This report covers the logistics sub-sectors that are currently attracting the most interest and funding. We'll discuss why these sectors are flourishing, the technological forces propelling them forward, and what investors should look for when assessing opportunities in this rapidly changing environment.

Disclaimer: Information provided in this article doesn't constitute investment advice. The information provided on this site is for general informational purposes only. It should not be considered as personalized investment advice or an endorsement of any particular financial product, security, or investment strategy. The information provided herein does not take into account your personal financial circumstances, goals, or risk tolerances.

Logistics Market Overview

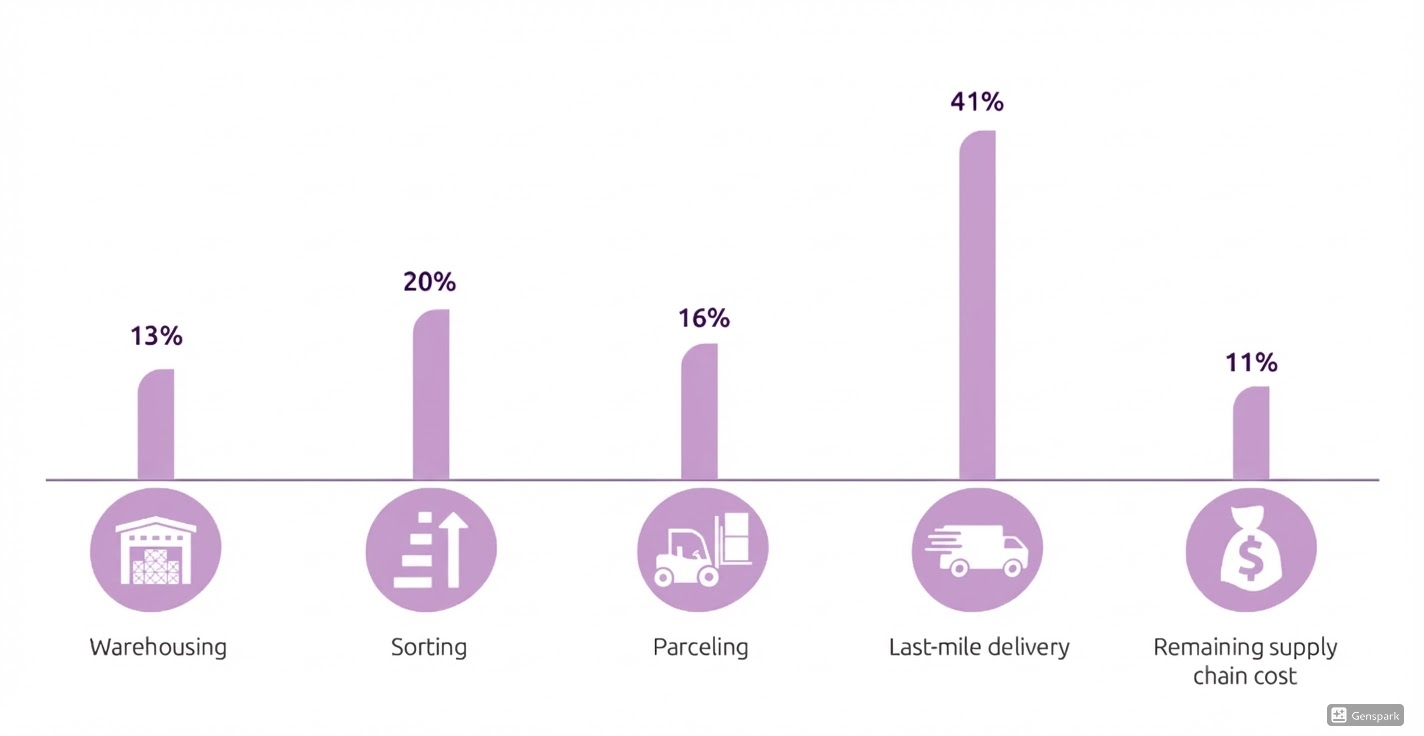

On the demand side, companies continue to pay for logistics on a massive scale. From a service perspective, customer expectations remain "two-day or faster" as the norm. Particularly in the last-mile, the burden of these costs is so significant that any sustainable unit-economics improvement scales to meaningful profit pools. For instance, Business Insider has referenced industry analysis showing that last-mile delivery accounts for 41% of overall logistics cost (a ballpark but handy heuristic for why route optimisation, depot density, and automation matter so much).

Software-Defined Logistics

Several current trends are reinforcing the shift to software-defined logistics:

- Electrification is transitioning from pilots to purchasing actuality in commercial fleets. The International Energy Agency reports an increasing availability of electric heavy-duty models and an explicit OEM focus on urban logistics applications (a proxy for last-mile and regional distribution).

- Automation is growing faster in warehousing, but the economics are not the same: even sophisticated grocers are retreading their automation footprints, as evidenced by Kroger's decision to shut a number of automated fulfillment facilities and move more delivery fulfillment to stores to make delivery faster and cheaper (a reminder that winners in automation strategies must be flexible in deployment and fast in payback.)

- AI routing and operations tools are evolving from dashboard analytics to decision-making systems. Currently, AI-driven decision making, real-time data, and hybrid delivery networks are key levers in last-mile optimisation. At the same time, regulatory and customer demands for decarbonisation are driving improved measurement and reporting.

Logistics Segments That Attract Investments

While the broader logistics industry continues to grow, capital is not flowing evenly across all sectors. Investment is increasingly concentrated in areas that solve specific pain points, such as the high cost of final delivery, the need for real-time visibility, and the demand for sustainable infrastructure.

Last-Mile Sector

The final leg of delivery, from a warehousing facility to the consumer's door (known as the last mile), remains the costliest and most complex segment of the supply chain. As mentioned above, last-mile delivery accounts for up to 41% percent of overall shipping costs. This inefficiency, coupled with increasing e-commerce volumes, has made the last-mile industry a focal point for investment.

Investors are particularly interested in businesses that can deliver at a lower cost per delivery while meeting consumers' expectations for speed. This includes:

- Crowdsourced delivery platforms: These models rely on gig workers to enable on-demand delivery and offer greater flexibility and scalability than traditional fleet models.

- Micro-fulfillment centers: Small urban warehouses that bring inventory closer to the consumer, significantly cutting down on transit time and cost.

- Automated delivery options: Still in their infancy, drones and autonomous ground vehicles (AGVs) are attracting significant venture capital, as they hold the potential to eliminate delivery labor costs entirely.

Investment thesis: Any technology or business model that can reduce last-mile costs by even a small percentage offers immense value at scale.

Example: Lalamove

- Founding year: 2013 (Hong Kong)

- Business model: Marketplace, asset-light

- Latest publicly specified venture round: Series F (2021), $1.5B (reported)

- Estimated valuation: Reported at around $10B

Why ranked here: Exceptional disclosed transaction scale, offer document profitability disclosure, and network effects in intra-city freight—core last-mile infrastructure in many markets.

Lalamove is a major, asset‑light logistics transaction marketplace connecting merchants with carriers, and its listing summary reveals scale to back a power-law network thesis: in 2024, it completed 779m orders, US$10.27B global freight GTV, and revenue increasing to US$1.593B (2024) with non‑IFRS adjusted profits of US$500.8m (2024).

Software and Systems Start-Ups

The logistics sector has traditionally been slow to embrace digitalization. Lots of processes still run on legacy systems, spreadsheets, and manual data entry. This digital lag has enabled a huge market for software and systems startups.

Interestingly, this segment of the market is currently quite small compared to the total logistics market. However, this small size is misleading. It represents a nascent market with strong growth prospects, largely driven by the industry's urgent need for digitalization.

Investors are flocking to start-ups that provide services such as:

- Transportation management systems (TMS): Today's TMS solutions are cloud-based and easy to use, enabling smaller carriers to operate their routes and loads more efficiently.

- Digital freight matching: Sometimes called “Uber for trucking," these apps connect shippers directly with carriers, cutting out traditional brokerage fees and trimming down empty miles.

- Visibility platforms: Monitoring goods in real time across multiple modes of transportation is now a necessity. Startups that consolidate information to provide a "single pane of glass" view of the supply chain are now in high demand.

Investment thesis: Inevitable adoption. Logistics companies that don't update their software stack will simply not survive, creating a continuing market for those that do.

Example: Shippeo

- Founding year: 2014 (Paris)

- Business model: B2B SaaS

- Latest publicly specified venture round: €40M financing (Oct 2022)

- Estimated valuation: unspecified

Why ranked here: Strong customer and shipment-scale disclosures.

Shippeo is a real-time multimodal transport visibility platform, and its financing announcement highlighted significant scale and ecosystem positioning. That is monitoring some 90 million shipments annually, solid customer adoption growth, and collaborations with leading supply chain software ecosystems and cloud infrastructure providers.

It's strong side? As sustainability reporting demands increase and trustworthy ETA and exception management are required, visibility platforms like Shippeo are moving toward operational automation, such as making data-driven decisions within shipper and 3PL workflows.

Warehousing

Despite the emphasis on software and asset-light models, physical infrastructure is still vital. But warehousing investment is becoming different. It is not just a matter of square footage anymore; it is about having smart, strategic capacity.

The need for smart warehousing stems from the need to bring inventory closer to the end consumer (to support next-day or same-day delivery) and the need to maintain additional safety stock to compensate for supply chain disruptions.

Investment opportunities in this space include:

- Cool chain storage: As demand for fresh food delivery and pharmaceuticals increases (see nuances of healthcare logistics), temperature-controlled warehousing is experiencing rising valuation.

- Multi-story warehouses: In land-starved cities, developers are building upwards. These large, complex buildings are capital-intensive to build and maintain, but they deliver unmatched customer proximity.

- Warehouse automation: Investors are backing facilities that are already equipped with automation or companies retrofitting existing space with automated storage and retrieval systems (AS/RS).

Investment thesis: WMS is now the cornerstone of modern logistics strategies. It is a physical real estate asset class that supports the digital commerce economy. The WMS market is expected to grow at a 19% CAGR from 2023 to 2030, according to Grand View Research. This growth is accelerating because of its ability to streamline business processes.

Example: Stord

- Founding year: 2015 (Atlanta)

- Business model: B2B, hybrid

- Latest publicly specified venture round: financing: $200M+ May 2025

- Estimated valuation: $1.5B.

Why ranked here: Recent large financing at a priced valuation, disclosed profitability claims, and clear evidence of scaled commerce volume—strong "platform + operations" profile.

Stord is a vertically integrated commerce enablement platform that combines software (OMS/WMS and consumer experience) with fulfillment and transportation. In May 2025, it announced securing $200M+ (equity + debt) at a $1.5B valuation, in conjunction with performance markers including 10x contracted revenue since 2021, sustained profitability in 2024, 30M+ packages delivered to ~11.5% of US homes in 2024, and ~$130M saved in parcel fees for brands in 2024.

Stord's edge is that omnichannel brands increasingly want a single operating-system partner to simplify split-3PL, and that scale and software can drive a margin flywheel (routing, carrier optimization, and higher warehouse utilization).

Air and Ocean

Air and ocean freight are the giants of global trade. Although these are mature industries, they are far from static. Investments in these fields tend to focus on modernization and sustainability. The market for digital fleet management solutions was valued at $20.58 billion in 2022, and it is expected to reach $79.82 billion by 2030. However, companies need to invest in advanced AI-based systems to stay competitive.

Investment opportunities in this space include:

- Green shipping: With environmental regulations becoming more stringent, significant investment is being made in alternative fuels (such as green ammonia or methanol) and energy-efficient vessel designs.

- Digital forwarding: AI-enabled freight forwarders are challenging traditional players with instant quotes, bookings, and tracking for air and ocean shipments, making a traditionally murky process easier to understand.

- Air cargo capacity: The decline in passenger flights during the pandemic has underscored the importance of dedicated freighter capacity. Investment continues to flow into converting passenger aircraft into freighters and modernizing air cargo terminals.

Note: Interestingly, the geography of logistics innovation has broadened. In 2023, North American startups accounted for the largest share of logistics VC (43%), and Indian startups also surged to match Europe's share. India's ascent correlates with the country's growing importance in supply chains and with support from both the government and investors for logistics technology (Delhivery, an Indian logistics company, raised substantial capital). We might also start seeing more emerging-market logistics startups addressing infrastructure issues with technology (for example, in Africa or Southeast Asia, startups are creating digital freight exchanges or using mobile technology to coordinate informal trucking).

Example: Forto

- Founding year: 2016 (Berlin)

- Business model: B2B, hybrid (tech-enabled forwarding)

- Latest publicly specified venture round: $240M at Series E (announced 2024 in company release)

- Estimated valuation: $2.1B.

Why ranked here: Scaled digital forwarding with a disclosed unicorn valuation and large 2024 round; ocean and multimodal digitisation remains a prime consolidation lane.

Forto is a mature digital freight forwarder with significant capitalization: it announced a $240M round at a $2.1B valuation, led by large growth investors, positioning it as a technology-and-service provider for end-to-end solutions across global transport flows.

Forto's strength lies in the fact that global forwarding is still largely fragmented and data-poor. Platforms that standardize documentation, visibility, exception management, and carbon reporting can capture market share and achieve a higher gross margin over time. This is particularly the case now that the requirements for reporting on regulations are extending further along supply chains.

AI Opportunities in Logistics for 2026 Investment

To determine where to invest, identify logistics areas where AI has the greatest impact.

Across developed-market logistics in 2026, the highest-probability profit pools for venture and growth equity are concentrated in software layers that:

- reduce labour and miles quickly

- monetise with recurring revenue

- avoid heavy regulatory exposure.

Note: Why does the transport sector need AI? The logistics landscape has grown increasingly complex in recent years. Factors such as shifting customer requirements, volatile fuel prices, extreme weather conditions, and capacity restraints can quickly derail the best-planned operations. Traditional approaches and human monitoring are becoming increasingly inadequate to handle these problems. As pressures mount for even faster delivery and lower operational costs, there is a need for smart systems that can anticipate disruptions, recommend adaptive response solutions, and, possibly, implement them with the requisite precision.

Fleet and Route Optimization, Dispatch Automation, and Telematics AI

Planning delivery routes efficiently is a tricky puzzle, but artificial intelligence and machine learning are making it quicker and more precise. The tools predict arrival times and delivery risks (traffic, weather conditions), and are even used to automatically communicate between shippers and carriers (e.g., to negotiate rates or book appointments). Enterprises implementing these AI-enabled solutions are experiencing tangible gains in operational efficiency and cost-effectiveness.

In 2025, HappyRobot secured a major Series B funding round to grow its AI agents that mimic natural-language conversations to automate the routine logistics tasks, including rate negotiation and appointment booking. This demonstrates strong investor confidence in AI solutions that complement existing transportation management systems rather than replacing them in their entirety.

The best opportunities in 2026 are AI solutions that:

- Integrate seamlessly with existing logistics systems.

- Offer low-cost, repeatable onboarding processes.

- Partner with established telematics providers, freight networks, or large third-party. logistics companies to accelerate market adoption.

Warehouse Automation, Robotics Orchestration, and Computer Vision

Using computer vision, machine learning, and AI, robots can navigate complex warehouse environments, efficiently pick items, and even conduct quality checks. These technologies need to work reliably in the real world: under different lighting conditions, through obstacles, and tightly integrated with existing hardware.

Look for companies that:

- Start with a single well-defined profitable use case, then scale across multiple warehouse functions.

- Have established, repeatable sales and deployment cycles, and unit economics that work.

- Partner with industrial automation firms and system integrators.

AI Supply Chain Planning and Digital Twins

A digital twin sits as an added layer of innovation on top of a traditional supply chain software solution, merging live data with simulation to enable enterprises to anticipate the impact of disruptions, optimize inventory positioning, and align decisions across functions. But there are many implementations which are simpler than that term suggests, often simulations rather than true, dynamic, real-time decision systems.

In 2026, focus on:

- "Narrow-first" solutions that demonstrate value quickly in specific use cases, then grow.

- Firms with robust ties to systems integrators and enterprise software ecosystems.

- Business models where channel partnerships increase rather than eat into margins.

Autonomous Logistics: Autonomous Trucks, Drones, and Last-Mile Robots

Some of the fundamental technologies in this sub-sector include sensor fusion (aggregating data from different sources), computer vision for object detection, route planning, safety systems, and massive simulation for testing. Proven safety, clear operational boundaries, and regulatory acceptance are the basis for commercial viability.

Look for opportunities in:

- Platform-enabling hardware technology (e.g., simulation, safety validation, remote operations, compliance tools) vs. full autonomy as a revenue generator in the immediate term.

- Strategic alliances with established logistics players with distribution and operational capabilities.

Autonomous delivery robots are increasingly considered vital to modern logistics systems because of their potential to address pressing challenges across the industry. Here's what makes them essential:

- Faster deliveries: Robots can operate 24/7, significantly reducing delivery times. For instance, urban delivery times have been slashed from 90 minutes to under 30 minutes in some cases.

- Operational savings: Robots are electric-powered, reducing fuel costs and maintenance compared to traditional delivery vehicles.

- Sustainability: Most delivery robots are electric, reducing carbon emissions and aligning with global sustainability goals.

- Reduced traffic congestion: By using sidewalks or bike lanes, robots minimize the impact on road traffic.

- Contactless delivery: Post-pandemic, it has become a priority. Robots provide a safe, hygienic solution.

- Logistics workforce gaps: The logistics industry faces acute labor shortages, particularly in delivery driver positions. Robots fill this gap, ensuring uninterrupted service.

- Navigating dense areas: Robots are designed to navigate crowded urban environments, making them ideal for short-distance deliveries on campuses and in cities.

- Integration with smart cities: As cities adopt smart infrastructure, robots can seamlessly integrate with systems like traffic management and IoT networks.

- Consistent performance: Robots are not affected by human factors like fatigue or errors, ensuring reliable deliveries.

Investor Mindset and Opportunities

Understanding where to invest is only half the equation. Understanding how to evaluate these opportunities is equally critical. The mindset of a successful logistics investor today is characterized by a focus on integration, sustainability, and resilience.

Evaluating Technology Adoption

Investors should evaluate not the technology in isolation, but rather the adoption barrier. The solution could be groundbreaking, but if it means changing the entire legacy system a logistics provider has relied on for 2 decades, expect long sales cycles.

The best opportunities are often in “overlay" technologies—solutions that layer on top of existing infrastructure and deliver value without requiring infrastructure rip-and-replace. API-first companies that plug seamlessly into major ERPs (Enterprise Resource Planning systems) and WMSs (Warehouse Management Systems) tend to gain traction faster.

The Sustainability Imperative

Environmental, social, and corporate governance (ESG) standards are now mandatory. Large shippers (retailers and manufacturers) are under enormous pressure to remove carbon from their supply chains. As a result, they are favoring logistics providers that can share data on carbon emissions and offer more sustainable options.

Look for startups that:

- Track and report on carbon.

- Optimize loads to minimize empty miles.

- Support the switch to electric fleets.

Resilience Over Efficiency

For many years, the supply chain mantra was "just-in-time", lean, efficient, and low-cost. But recent years of disruption have shifted focus to "just-in-case." Companies are willing to pay a premium for resilience, so investors need to seek out businesses that can be flexible.

Now, investor sentiment is still cautious but positive for the right opportunities:

- Investors now care about unit economics and a clear path to profitability. The “growth at all costs" era in logistics tech is giving way to questions about whether a startup can actually earn money (which is healthy for the sector).

- There's a crevice to be filled in solving niche but painful problems in logistics. For instance, software that orchestrates returns logistics (a space expanding with e-commerce) or AI that streamlines customs paperwork can create profitable niches.

- Integration, platforms: The highly fragmented logistics world (think myriad small trucking firms, warehouses, etc.) is seeking answers with solutions that can integrate. Startups providing platform approaches that link these fragments (and build network effects) will be closely watched.

The logistics startup landscape in the immediate future will be about "enablers" and "niche providers" that complement or fill gaps left by larger players. Supply chain resilience and efficiency remain front of mind for enterprises, making startups focused on visibility, flexibility, and cost control well-positioned. We might also see a pickup (more disciplined) in logistics funding if macro conditions improve (meaning interest rates stabilize and global trade starts moving).

Look for:

- Logistics AI startups using generative AI to develop smarter decision tools for routing and planning, logistics customer service bots, etc.

- Companies are focusing on automation across software and hardware, including those that coordinate robots in warehouses or autonomous yard vehicles at distribution centers.

- Logistics fintechs lending to and insuring goods on the move, supply chain financing platforms, etc. These services are essential to complicated global commerce.

Final Word

The future of logistics will be built by those who can marry the physical movement of goods with digital sophistication. If they concentrate on the above-identified portions of the industry, namely last-mile, software, AI, SaaS models, warehousing, and modernization of global freight, they can position themselves on the leading edge of this increasingly critical aspect of the economy.

There are plenty of opportunities for the shrewd investor. Be it a SaaS product simplifying freight bookings, an AI company forecasting supply chain disruptions, or a sustainable last-mile delivery provider, the spaces seeing interest today share a common characteristic: they address complex challenges with scalability and intelligence.

Roman Zomko

Other articles